by admin1124

by admin1124Calculate your car loan interest for early settlement using Rule of 78

“Car loans cannot be transferred from one party to another. Therefore, when an owner sells his car, he will need to fully pay off the loan before the ownership transfer. Car buyers usually finance their purchase with a loan of five years or longer, but because most of them will sell their cars before that, early redemption of car loan is commonplace.

Early redemption amount for car loans in Singapore is calculated based on the Rule of 78, which is a method of allocating the interest charge on a loan across its payment periods. More interest charge is allocated to earlier payments compared to the later ones. Because of this, paying off a loan early will result in the borrower paying more interest overall.

Because the banks need to cover their administrative costs and commission already paid out, car owners who early redeem their loans are further penalized with a charge of 20 percent of the unpaid interest; the bank will only rebate the borrower 80 percent of the unpaid interest instead of the full sum.

Banks usually further charge an Early Settlement Penalty, but in our below example, we will ignore this portion.

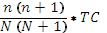

Now, the formula for Rule of 78.

R =

Whereby:

R represents the unpaid interest

n represents the balance loan period expressed in months

N represents the original loan period expressed in months

TC represents the total amount of interest payable over the loan period

When doing an early redemption on a car loan, the amount to pay is:

Initial loan amount + total interest – instalments already paid – 80 percent of unpaid interest.

Let’s say you have a five-year loan of $50,000 at three percent interest that you wish to fully pay up after 20 months. Assuming the bank uses the Rule of 78 to calculate the interest rebate, with a 20 percent penalty on the rebate for early repayment.

Loan amount = $50,000

Interest rate = 3% per annum

Total interest to be paid = (3% x 5 years x $50,000) = $7,500

Period of finance = 60 months or 5 years

Monthly instalment = ($50,000 + $7,500) / 60 = $958.33

Number of instalments paid = 20 months

Total amount already paid for = $958.33 x 20 = $19,166.67

Unpaid interest according to Rule of 78 = [40(40+1)] / [60(60+1)] x $7,500 = $3,360.66

Here, 40 represents the number of months remaining of the bank loan that is unpaid, and 60 is the original number of months of the bank loan. The amount of $3,360.66 is the unpaid interest on the 40 months from early termination of the loan.

80% of unpaid interest = 0.8 x $3,360.66 = $2,688.52

Loan redemption amount = $50,000 + $7,500 – $19,166.67 – $2,688.52 = $35,644.81

That is, initial loan amount ($50,000) plus total interest ($7,500), deducting the instalment amounts already paid for ($19,166.67), deducting the 80 percent of unpaid interest ($2,688.52), resulting in the loan redemption amount ($35,644.81).”